In recent times, the investment arena has witnessed the rise of investment services known as automated Robo-advisors. These platforms create a middle ground between working with a financial advisor and choosing to go it alone.

Robo-advisors offer various types of services, investments, and extra features, such as automatic rebalancing and tax-loss harvesting, at a cost much lower than a financial advisor would charge.

Nevertheless, considering that a plethora of these Robo-advisors have popped up and offer similar services, features, and benefits, it is increasingly difficult to find a platform that best suits your needs.

Thankfully, this article will help cut through the noise. To achieve this, we have taken the time to compare Betterment and Personal Capital, two of the most popular options on the market when looking for an investment platform.

By the end of this article, you should have a better idea of which Robo-advisor platform best works for you. Speaking of which, if you are interested in knowing the difference between a Robo-advisor and a traditional financial investor, read this article.

Let’s begin!

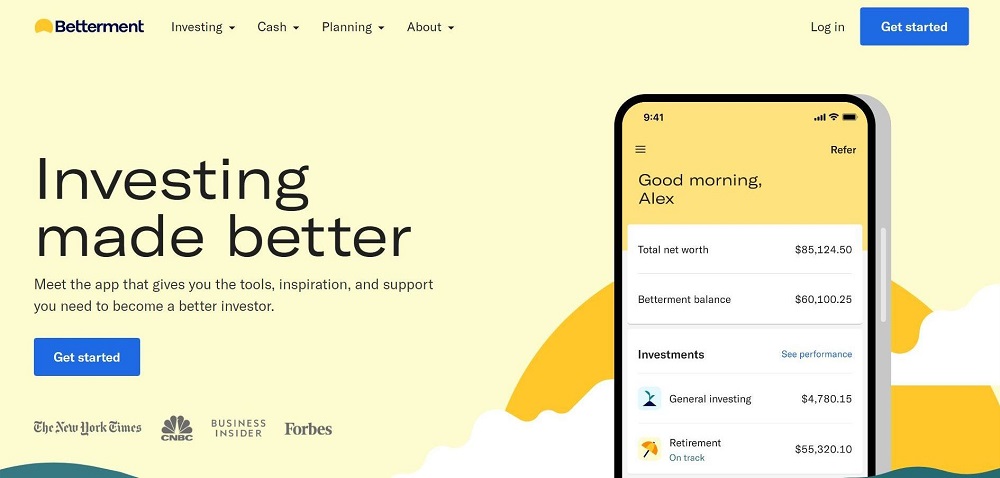

Betterment

Betterment is for new investors looking to start their investment journey. With that in mind, it has a platform and an autonomous investing tool that doesn’t require any additional effort on the part of the user.

All you have to do is provide basic information about yourself, your investment and financial situation, and of course, your financial goals. What you get in return is a flexible and tailored investment plan for your needs.

Betterment Accounts

- Traditional, Roth, SEP, and Rollover IRAs

- Individual and Joint taxable accounts

- Trust accounts

- High-interest savings accounts

Betterment offers five different portfolio types to choose from. They are all created with the Modern Portfolio Theory principles. These portfolios include:

- Standard portfolio of bond ETFs and globally diversified stock

- Socially responsible investing portfolio consists of high-interest holdings that score well on social and environmental impact (note that investments may not meet standard requirements for this theme).

- Goldman Sachs Smart Beta portfolio that seeks to outperform the market

- Income-focused bond portfolio of BlackRock ETFs

- “Flexible Portfolio” of standard portfolio asset classes weighted by user preferences

The accounts in Betterment are dynamically rebalanced when they begin to deviate from their financial goal allocations. Additionally, when a portfolio’s target date draws nearer, the portfolio becomes conservation with the primary goal of preventing major losses and locking in gains.

Features

Betterment offers its clients free financial planning tools to help provide a comprehensive analysis of their previous investments before they create an account. It also offers flexible goals by providing goal planning resources such as coaching. The investment account interface is designed to support enhanced portfolio flexibility.

For clients who want a bit more, the Betterment premium plan offers a financial advisor at any moment at no extra charge. It is important to note that the premium plan charges a 0.4% management fee over the 0.25% management fee charged by the standard plan.

With Betterment, users have two plans to choose from: the Digital plan, which comes with an annual fee of 0.25% and no account minimum balance. On the other hand, the Betterment Premium plan requires a $100,000 minimum balance with a 0.40% annual fee.

With the Digital plan, you get personalized advice on the assets you hold outside Betterment. You can also get guidance on life events such as retirement, having a child, or getting married. Additionally, you also get ETFs in the Betterment portfolios that come with management fees within the range of 0.07% and 0.15%.

In contrast, Personal Capital allows customers to access financial advisors on the paid version. Investors with a minimum of $200,000 investment will get two financial advisors. There are no minimum investment balances with the free version of Personal Capital. However, the investment management variant requires an investment of at least $100,000.

For those looking to limit their tax liabilities, Personal Capital uses numerous strategies to minimize income taxes generated from investments. These strategies include tax-loss harvesting and tax allocation. It also uses tax efficiency strategies like not investing in a mutual fund as they are more likely to generate capital gains.

Betterment provides easy steps to set goals, with each monitored separately. This enables you to set up many goals with varying target dates. This means portfolios tend to vary considerably. As a user, your asset allocation is displayed in different colors, with equities shown in green and fixed income in blue.

Interested in how the pandemic affected your investments? Read here.

Personal Capital

Personal Capital is created with a focus to provide investments for individuals with higher investment funds. It is also designed for the investor who wants a Robo-advisor but still wants access to a human financial advisor just in case the need arises.

The accounts offered are geared towards higher balances, which is evident in the number of custom and prebuilt investment portfolios.

Personal Capital Accounts

- Individual as well as joint taxable accounts

- Traditional, rollover, SEP, and Roth IRAs

- Trusts

- 529 college plans

- Advice only employer-sponsored retirement plans

Personal Capital offers three distinct investment services based on how much you intend to invest initially. These include:

- Private Client services, which are offered to investment assets with a value of more than $1 million

- Wealth Management services offered to investment assets with a value between $200,000 and $1 million

- Investment Services offered to investment assets up to $200,000

Personal Capital operates a customizable investment strategy based on a customer’s general financial situation and personal goals. These can include medium-term investment goals that suit the investor’s current situation, such as financing education or purchasing a home.

Personal Capital uses a tactical weighting approach alongside the indexing of United States equities. This allows it to maintain an evenly weighted exposure in stocks and other sectors.

The portfolio created is based on the MPT or Modern Portfolio Theory, which includes a diverse range of about 100 stocks for tactical weighting and tax optimization. Also included in the investment portfolio are small-cap index ETFs.

The portfolio created is always rebalanced to ensure that asset classes are kept within your allotted target. They are also monitored daily to ensure everything goes according to plan.

Getting a Personal Capital portfolio means that you will have six asset classes in your portfolio, including:

- International stocks

- US stocks

- International bonds

- US bonds

- Cash

- Alternative assets such as REITs or real estate investment trusts, gold and energy, help to hedge against inflation

With Personal Capital, you aren’t required to deposit your investment portfolio funds. Instead, your account is held in Pershing Advisor Solutions, which is made up of over $1 trillion in clients’ assets. With this, you can check on your account through the Pershing online platform located on the dashboard. You can also receive e-statements from both Pershing and Personal Capital.

Features

Personal Capital’s platform has investment and budgeting applications. This service is suited to those who get the wealth management service. The free version of this platform includes goal and budgeting settings. It does this by incorporating strategies to help you reach your investment goals. This also includes providing support for your retirement planning, reports on spending and income, as well as managing your investments.

Personal Capital has a fee analyzer that allows users to recognize any hidden investment fees. It also recommends alternative investments to reduce or eliminate the fees. You can also get an investment check-up, which is a tool that helps analyze your portfolio and offers financial advice on how to make improvements to reach your investment goals.

The retirement planner also comes with a Retirement Calculator that helps you plan for your retirement. It does this by tracking your progress against the goals you have made. You can also calculate your rental income, pensions, and Social Security benefits. The retirement planner also works for budgeting for a college education and other functions.

Conclusion

When it comes to choosing a Robo-advisor to manage your investments, it is not a decision that should be taken lightly. You have to ensure that whichever broker or platform you choose is one that strongly aligns with your goals. It also has to offer you valuable features that you can use to make your investment journey a lot better.

The decisions you make between these two platforms typically depend on what you want from a Robo-advisor. For example, if you are just starting your investment journey, you would be more inclined to choose a platform that allows you to access the most effective and scenario-relevant investment options. It should also offer a low minimum. If this sounds like you, Betterment is the better option for you.

Conversely, if you are already some years into your investment journey or looking to invest a large sum in your portfolio, you most likely wouldn’t mind paying a higher price for an improved service. In this case, Personal Capital might have features and tools for your investment options. We also have an article laying out the pros and cons of Betterment Vs Fidelity.